Blog

Acclaim Magazine Interview with Tate Haymond, Chief Revenue Officer, d1g1t

Ready to Transform Your Portfolio Management? Join Our Exclusive Webinar

RIA Channel Interview with Tate Haymond, Chief Revenue Officer, d1g1t

From Data to Decisions: Elevating Wealth Management through Analytics with Dr. Dan Rosen

Essential Tech Efficiencies RIAs Should Embrace to Stay Competitive

d1g1t Recognized in the Gartner® Market Guide for Wealth Management All-in-One Advisor Desktop Platforms

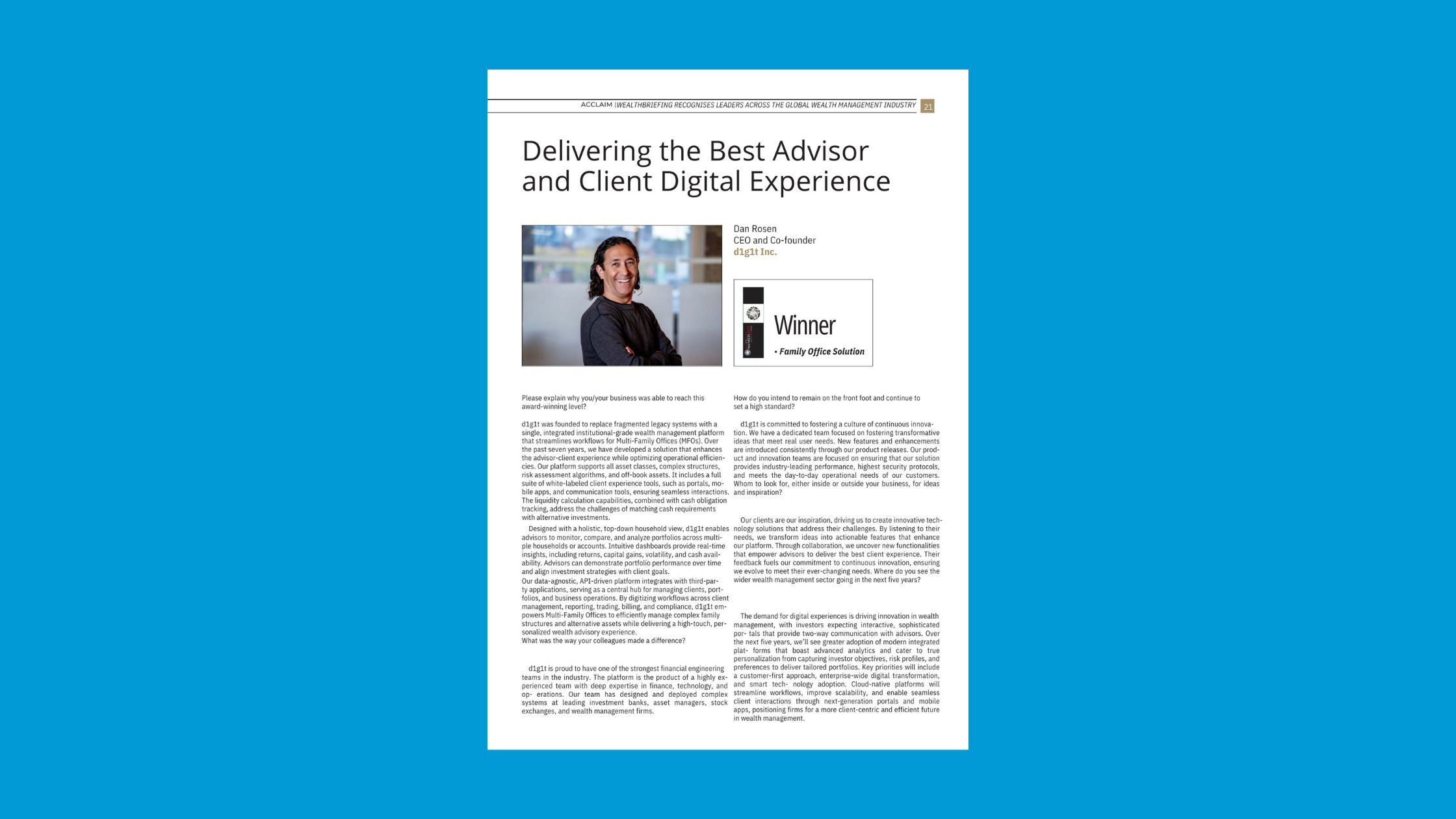

Acclaim Magazine Interview with Dr. Dan Rosen, CEO, d1g1t

Navigating Uncertainty: Diversification, Duration, and Goal-Based Optimization in 2025

How First Atlantic Private Wealth Improved Wealth Management with d1g1t

d1g1t Version 5.1: Enhancing Wealth Management Through Technology

Why Multi-Family Offices Are Falling in Love with d1g1t

Understanding CSA Regulatory Requirements for IBOR and How d1g1t Simplifies Compliance

Ready to take the next step?

See how d1g1t Delivers the Best Advisor and Investor Experience.